Credit scores are numbers that evaluate your creditworthiness and financial health. They are issued by credit bureaus or other consumer reporting agencies and are used by lenders to evaluate consumers for credit approval, terms and interest rates. In the U.S., there are three main credit bureaus: Equifax, Experian, and TransUnion. Most credit scores are issued by one of these three. A credit score is generated when a bureau or other reporting agency runs consumer information through a scoring model; FICO is one such system. Read on to learn more about the credit bureaus, the Difference Between FICO® Score and Credit Score and alternative scoring models.

All FICO® scores are credit scores, but not all credit scores are generated by the FICO scoring system.

Glossary

Credit Score: a numbered rating that evaluates your creditworthiness based on your financial history

The Credit Bureaus: Three private credit bureaus (Experian, Equifax, and TransUnion) that aggregate information and create a credit report and score. No other private credit reporting companies are considered “bureaus.”

Credit Reporting Agency: A private company that aggregates information and creates a credit report and score but is not one of the three main credit bureaus.

FICO: a brand acronym for the Fair Isaac Corporation

FICO® Score: a branded credit score created by FICO

VantageScore: a company name and branded credit score

The FICO Predictive Scoring System

FICO stands for Fair Isaac Corporation. FICO was founded in 1956 by engineer William R. Fair and mathematician Earl Judson Isaac. Together they created a scoring system designed to rate consumers based on their financial behaviors. After pitching the system to the top fifty lenders, it became a successful and popular way for institutions, landlords, and more to evaluate a consumer’s financial fitness.

FICO® Scores range from 300 to 850, which differs from industry-specific scores that range from 250 to 900.

A credit score is considered a FICO® Score when it uses the proprietary scoring system developed by Fair and Isaac.

The version of the FICO scoring systems used today was developed in 1989. Fannie Mae and Freddie Mac began using the system in 1995. Today 90% of lenders use FICO® Scores to decide credit approvals, terms, and interest rates.

VantageScore is An Alternative to FICO

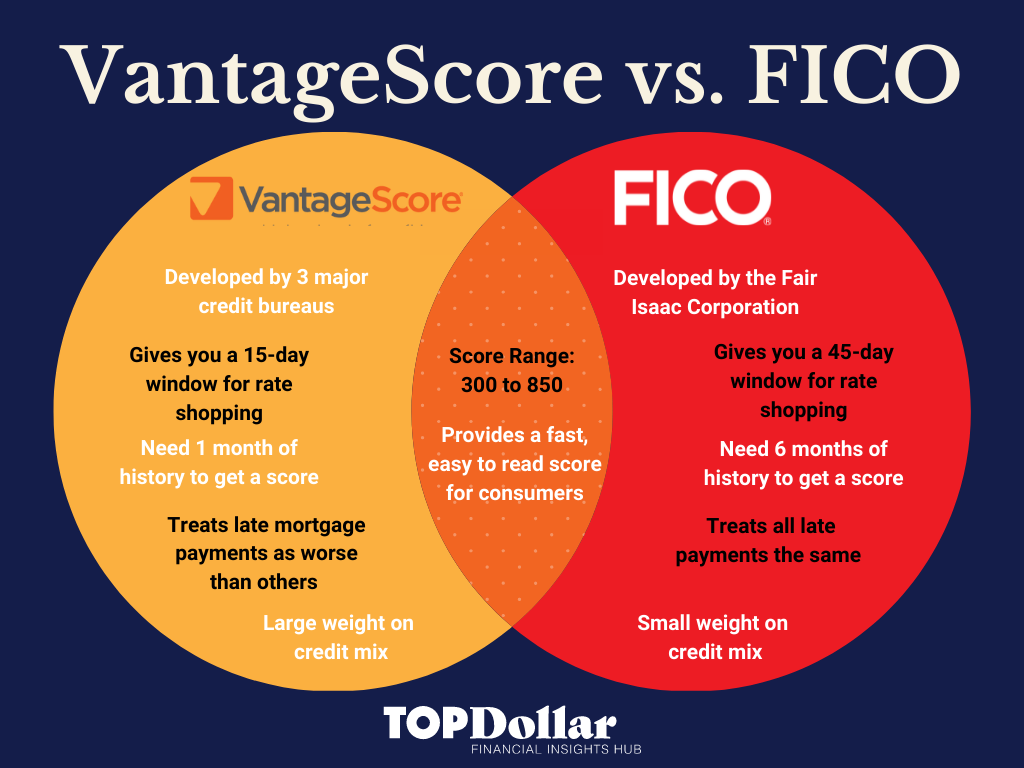

Another scoring model called VantageScore is a well-known alternative to the FICO model but still isn’t as popular or widely used. As a competitive alternative to FICO, the VantageScore was developed by three major credit bureaus, Experian, Equifax, and TransUnion.

In 2006 the bureaus jointly funded the development of the VantageScore brand. They profit from the development of this scoring system and its use by other reporting agencies but still use versions of the FICO model for their credit reports.

Notably, all three credit bureaus use versions created by FICO to work with each credit bureau’s credit reports. There are many different versions of the FICO scoring model for different types of credit pulls. FICO 8 is the most common.

The 3 Main Credit Bureaus

A credit bureau is an agency that aggregates information and creates a credit report that is then scored using a system like FICO or VantageScore.

Experian, Equifax, and TransUnion are the three main credit bureaus that provide credit score information to lenders.

- Experian

- Equifax

- TransUnion

FICO® Score Variations Used by The Credit Bureaus

| FICO Model | Description |

| FICO 9 | Newest version. Not widely used. |

| FICO 8 | Most common. Used for Auto and Bankcard lending. |

| FICO 5 | Used by mortgage lenders. Built on data from Equifax. |

| FICO 4 | Used by mortgage lenders. Built on data from TransUnion. |

| FICO 2 | Used by mortgage lenders. Built on data from Experian. |

Source: ValuePenguin

Because the bureaus and their applications of the FICO scoring model are so well known, people often refer to them simply as “The Credit Bureaus” and all credit scores as “FICO.”

It’s helpful to know what model was used to calculate your score, especially when getting it from a third-party website. All FICO® Scores are credit scores, but not all credit scores are generated by the FICO scoring system.

FICO® Scores will bear the copyright symbol on official documents.

Note: If a score is called a “FICO Score” but does not bear the copyright symbol, it might be a copycat, and the agency may not be reputable.

The Difference Between VantageScore and FICO

Both FICO® Scores and VantageScores serve the same purpose: to help lenders evaluate a consumer’s creditworthiness. The scores are used for credit approval, terms and interest rates.

Both Fico and VantageScore ratings range from 300 to 850, and higher scores are better and make it easier to qualify for competitive financing offers that can save you thousands of dollars.

Initially, VantageScore used a different range: 501 to 990 but changed to the current model after version 3.0 of its scoring system.

Both provide consumers and lenders with a fast and easy-to-read way to evaluate their credit. However, VantageScore can do so with much less information than FICO. You only need one month of information to get a VantageScore vs. six months for FICO.

Both give consumers a rate shopping window, but FICO’s are more generous. During this window, all hard credit checks for the same type of loan in any one of those categories count as one inquiry.

VantageScore puts more weight on late payments if they are for a mortgage. Whereas FICO treats all late payments equally.

FICO also deprioritizes the credit mix, while VantageScore gives it greater consideration.

Neither FICO nor VantageScore is particularly transparent about how public records information or adverse accounts are weighed in their algorithms.

Why Are My Credit Scores Different?

An inconvenient reality of any credit scoring system is that it is only as accurate as the information obtained by the bureau and put through the scoring algorithm. Scores can vary even between entities that use the same scoring system if they have access to different financial information. If some information is provided to one bureau and not another, that will affect your score.

Different variations of the FICO® Score weigh some variables higher than others relative to the model’s intended purpose. So, If the same information is run through FICO variants, the results can be different.

The same is true when FICO® Scores are compared to VantageScores. They won’t be identical because the systems weigh the information differently.

How Can I Build My Credit Score?

The best way to have healthy credit is to practice good financial habits. Your score will fluctuate, but small changes shouldn’t significantly impact your overall creditworthiness if you consistently make good choices like following a budget and keeping your debt-to-income ratio within reasonable limits.

Healthy Habits For Your Credit

- Regularly monitor your credit score for unusual changes

- Dispute inaccurate information

- Follow a budget

- Keep debt-to-income ratio within reasonable limits

- Pay bills on time

- Reorganize and pay down debts on time

- Maintain a diverse credit mix

Today, sites like Annualcreditreport.com offer the ability to check all three bureau scores, plus your FICO® Score, and may even create a separate aggregate or average score. Some credit cards or financial services offer free credit monitoring as well.

Can I Repair My Credit When I Have Too Much Debt?

If you are struggling with debt, it’s crucial to get that under control before focusing on your credit score. Solutions like debt consolidation can help you reorganize and pay down your debt. As your debt decreases, your creditworthiness can improve. Then you can focus on building your credit score through healthy habits to achieve your financial goals.