Have you finally caught up on your past-due loan payments? Perhaps you just completed debt consolidation and were able to pay off your debt.

If you have been working hard to pay off or consolidate your debt it can be frustrating to see your credit score drop or stay stuck. Unfortunately, when it comes to debt consolidation, a temporarily lower credit score may be a part of the process.

Credit repair is straightforward but requires patience, discipline, and a reliable strategy. These examples will show you how you can repair your credit in 6 steps and adopt lifelong habits that will help you maintain a good financial reputation.

Repair Your Credit in 6 Steps

Steps 1 to 3 are the foundation of credit repair. It’s important to take care of these steps first before moving on to steps 3 through 6.

- Dispute inaccurate credit report information

- Make a budget

- Reorganize or pay down debts

| PROCEED TO STEPS 4 THROUGH 6 WHEN: |

| You have no outstanding late payments You have a debt repayment plan with manageable monthly payments that you can afford You have made a budget and are able to stick to it consistently |

- Adopt responsible credit habits

- Build new types of credit

- Pay bills on time and watch credit gradually improve

Good credit habits work best after you have taken the time to get your debt under control. The later steps of credit repair usually involve responsibly taking on new debt which shouldn’t be done until you have addressed past due balances through debt consolidation options.

Step 1: Disputing Inaccurate Credit Report Information

Mistakes happen and if information on your credit report is not correct, you have a right to dispute the charges and have them removed.

Under the Fair Credit Reporting Act, credit bureaus such as Experian, Equifax and TransUnion are required to investigate your credit report dispute. If they do not respond within 30 days of the dispute the item must be removed from your report. In some cases, a credit bureau will respond within 30 days and request more documentation. This can extend the dispute timeline, usually not more than 3 to 6 months.

How to Dispute Thing on Your Credit

1. Request credit report

You are allowed to ask for one free credit report each year. You can order the report directly from the credit bureau or use a third-party site. Often banks and credit card companies will offer monthly credit reports as a complimentary service.

2. Look for errors

Carefully review your report and identify the information you would like to dispute.

3. Fill out a credit bureau dispute form

The easiest way to file a dispute is to fill out the online forms available on the credit bureau website. Some third party companies and credit repair services can do this for you.

Here are some quick links to help you get started:

| How to file a dispute with Experian | Experian dispute form |

| How to file a dispute with Equifax | Equifax dispute form |

| How to file a dispute with TransUnion | TransUnion dispute form |

Can you dispute accurate information on your credit report?

You have a right to dispute any information on your credit report to check its accuracy. A dispute requires the credit bureau to review the information in a timely fashion to ensure that it is correct. If the bureau does not respond to a dispute within 30 days the item will be removed from the report. However, having something removed from your report does not mean that you are not responsible for paying the debt.

Step 2: Make a Budget

This may seem like finances 101, but it’s a critical step. Thinking about your budget isn’t enough. You need to put pen to paper or in this case, use a budgeting spreadsheet that honestly tracks your monthly input and output.

Record all of your income and expenses in a trackable format and sort by category. Then subtract your expenses from your income to see how much is left over each month.

Typically, anything that is leftover would be saved and invested, but if you are deeply in debt, you may want to consider using this money toward paying down past due balances, making extra payments, lowering the balances on high interest debt.

If you get a negative value, then you are living beyond your means and should consider increasing your income, cutting your spending, and reorganizing your debt.

The goal is to understand exactly where your money comes from and where it goes so that you can calculate how much money you can reasonably put toward paying down your debts.

Step 3: Reorganize and Pay Down Debts

This step is especially important if you are behind on your debt, have monthly payments that are more than you can afford, or have debt that is ballooning out of control due to high interest rates.

The steps you take to get your debt under control will depend on how far behind you are, your budget and could include debt consolidation.

Lower Credit Utilization

If you aren’t behind on payments but have maxed out or used a high percentage of your credit limit you’ll want to pay down those balances and aim for a credit utilization of 35% or less.

Improve Debt to Income Ratio

Your Debt to Income Ratio is the percentage of your gross monthly income that is used to pay back your debts. It is important because it helps lenders determine if you are living beyond your means.

Although this number does not directly affect your credit score, it does help determine your eligibility for new credit, which is something you might need as you work to improve your score.

Learn more about why your debt-to-income ratio matters and what you can do to improve it.

Step 4: Adopt Responsible Credit Usage Habits

Demonstrating that you can responsibly use your credit and make regular payments on your debts is one of the best ways to repair your credit. Use these daily, monthly, and yearly tips to show lenders that you are a responsible borrower.

Begin by choosing an existing credit line with a reasonable interest rate that you can use regularly. Cards credit with cashback and mile rewards can be great for this. The goal is to use the card for daily expenses and pay it back each month. With most cards, you can set up autopay and pay down the balance or a particular amount on a regular schedule.

| Daily | Use a Credit Card for daily or recurring purchases |

| Monthly | Pay down all or almost all of the balance |

| Yearly | Request a credit limit increase, add new lines as needed |

Will zeroing my credit card every month improve my score?

A zero balance on your credit card, because you pay your balance in full, may not affect your score depending on when the payment was made

The reason: your balances are reported at various times throughout the month and usually coincide with your statement date. For this reason, your credit card balance might not be $0 on the day your credit card issuer reports it to the credit bureaus.

For example, if you made a $300 purchase on the 5th of the month and pay it in full on the 15th of the month, but your credit report was updated on the 10th, your report won’t show a zero balance. The timing of your payments can affect your score. This is not something you should worry about.

As long as you are continuing to make payments and your utilization is low, it is not necessary to have a zero balance. In fact, some lenders prefer a non-zero balance because it means you are paying interest, which is how they make money.

How can I get a credit card if I have bad credit?

If you don’t have a credit card and have bad credit, there are options available to you. You may be able to open a secured credit card or become an authorized user on a joint account. Credit cards for bad credit often have lower limits, higher fees and interest rates, but you’ll be able to use the card the same way to demonstrate that you can responsibly use credit and pay it back on time.

When can I ask for a credit limit increase?

It’s best to wait 6 to 12 months after opening a credit line to ask for an increase. If you have been paying regularly on your credit card you can ask for an increase once a year.

Ask for a credit limit increase when:

- Your income increases

- Your credit score has increased

- You have paid regularly on a line of credit for 6 to 12 months

Do not ask for a credit limit increase when:

- You recently requested increases on other lines

- Your score has declined

- You’ve taken a lower-paying job

Step 5: Build New Types of Credit

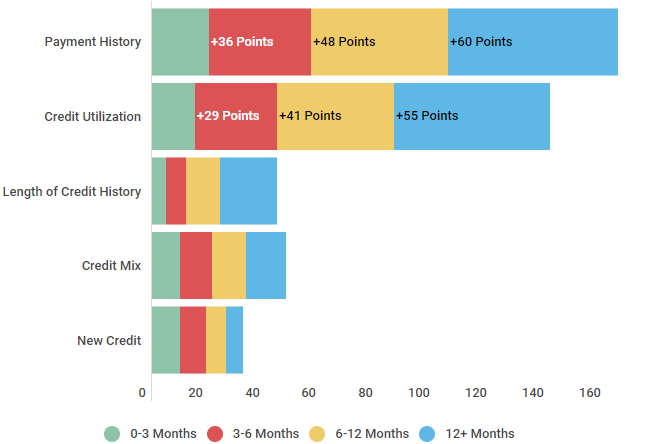

Credit mix generally makes up 10% of your credit score. Credit bureaus like to see a diverse mix on your report because it shows them that you can manage different types of credit. In addition to credit cards here are some other types that can reflect positively on your credit score if managed responsibly.

- Utility bills

- Auto loans

- Home mortgage

- Student loan payments

- Secured or unsecured personal loans

- Loans from non-profit lenders or credit unions

Opening new accounts and paying on time can have a big impact on your credit. Expect to see results in 6 to 12 months.

Step 6: Pay Bills on Time and Watch Credit Gradually Improve

Stay organized by setting up automatic payments and regularly update your budget when input or output changes. Payment history usually makes up 35% of your credit score, so paying on time is a must.

You can monitor your credit monthly with a credit score service. Some services are free and have simulators that use the current information on your report to estimate how changes will affect it. Keep in mind that the changes are hypothetical and most credit score companies partner with lenders to show you ads for new credit cards and loans.

If you already have a good credit mix, It’s important not to take on new debt that you don’t need. Step 6 is about managing the debt you already have.

How Long Does Credit Repair Take?

Repairing your credit and practicing good credit habits isn’t about instant gratification. For most of us it involves a lifestyle change and a big shift in how we manage our money. Consumers who have demonstrated fiscal responsibility over a long period of time have higher scores and better reputations.

Source: Credit Sesame

While it can take as little as 30 days to see improvements to your score, more significant improvements happen over time. Derogatory marks can stay on your report for 7 years, though their weight in affecting your score lessens over time.

Ultimately, practicing good financial habits consistently over time is the only way to build good credit.

Learn More:

What is Credit Repair and Why Do You Need It?

7 Reasons You May Need Credit Repair