If you’ve been making payments for over a year and your balances still aren’t moving, a debt consolidation loan could be worth a serious look. It rolls what you owe into one fixed monthly payment, usually at a lower interest rate than your credit cards carry.

This guide covers when a debt consolidation loan makes sense, how it compares to other options including debt relief programs, and what the real costs look like.

When Is Debt Consolidation a Good Idea?

Debt consolidation works best when you have a clear understanding of the types of debt you’re carrying and responsible financial habits to back it up. It tends to be a smart move when you can check a few of these boxes:

- You qualify for an interest rate that’s lower than what you’re currently paying. This is especially important when considering consolidation loan options. If a consolidation loan does not reduce your interest rate, you are not saving money, you are just reorganizing it.

- You have multiple accounts to manage. Keeping track of several due dates, minimum payments and interest rates across different accounts leaves a lot of room for error.

- Your credit score is in good shape. A stronger credit profile gives you access to better loan terms, which is what makes consolidation worthwhile.

- You have a stable income. Consolidation works best when you can commit to a consistent monthly payment over the life of the loan.

Types of Debt Consolidation: Loan vs. Debt Relief Program

There are two main ways to consolidate debt, and which one makes sense depends on your credit profile, income and how much you owe.

Debt Consolidation Loan A personal loan that pays off your existing balances, leaving you with one fixed monthly payment at a set interest rate and term. Works best if you qualify for a rate lower than what you’re currently paying and have stable income and a solid credit score.

Debt Relief Program Also called debt resolution, a company like Accredited Debt Relief works with creditors to target what you owe, lower your eligible monthly payments and set up a new repayment timeline. It can be a better fit for people carrying significant unsecured debt who are struggling to qualify for a loan or keep up with minimum payments.

When a Debt Consolidation Loan May Not Be a Good Idea

If you have a history of missed payments, limited or unstable income or a poor credit score, it may be difficult to qualify for a consolidation loan with a reasonable interest rate. Even if you do qualify, the monthly payment may still be more than your budget can handle, leaving you back in the cycle of making only minimum payments and barely making a dent in what you owe.

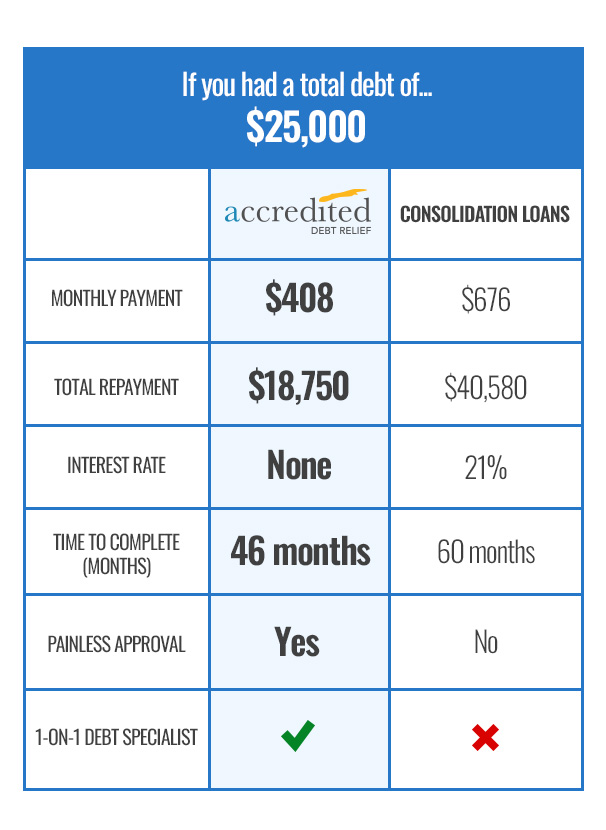

The Cost of a Debt Consolidation Loan vs. Other Options

The best way to understand the cost of a consolidation loan is to examine how much is paid in interest over the loan’s life and compare it to the savings in other options.

*The total repayment amount includes fees. Fees vary by state and are based on a percentage of your enrolled debt at the time of starting and range from 15%-25% of your enrolled debt.

What Will a Debt Consolidation Loan Actually Cost You?

The cost of a debt consolidation loan comes down to two things: your repayment term, interest rate and your fees. A longer term may lower your monthly payment but cost more in interest over time. A shorter term may do the opposite.

On the fee side, most loans include an origination fee of 1% to 6% of the loan amount, deducted before you receive your funds. Watch for annual fees, late fees and prepayment penalties as well. Always read the fine print before signing.

Weigh Your Options Before Applying for a Debt Consolidation Loan

Every situation is different, and the right option depends on your specific financial picture. Reach out to a Consolidation Specialist at Accredited Debt Relief for a free consultation before you decide.

The information on this site is provided as a general resource and does not constitute legal, tax, or financial advice. While Accredited Debt Relief makes every effort to ensure accuracy, this content, including any third-party sources referenced, should not be the basis for any financial decision. For guidance specific to your situation, we recommend consulting a qualified professional.