Keeping up with multiple credit card payments every month is stressful enough. Add in varying interest rates, different due dates and balances that barely seem to budge, and it is easy to feel like you’re working hard without making real progress. Consolidating your credit card debt could change that picture.

This article walks through what debt consolidation is and the key signs it could be the right move for you.

What Does It Mean to Consolidate Credit Card Debt?

Debt consolidation combines your credit card balances into a more manageable structure — whether that’s a lower interest rate, a single monthly payment, or a reduced total balance. There are three main paths to get there, and the right one depends on your credit profile, how much you owe and what you’re working toward.

Balance Transfer Card

A balance transfer card lets you move existing credit card debt onto a new card, often with a 0% introductory APR for a set period. This can be a strong option if you have good to excellent credit and can realistically pay off the balance before the promotional rate expires.

Personal Loan

Using a personal loan to consolidate debt means paying off your credit card balances and replacing them with a single fixed monthly payment at a set interest rate. This option tends to work best when:

- The loan rate is meaningfully lower than your current card APRs and

- You have steady income to support consistent repayment

Keep in mind that not all applicants will qualify for the lowest available rates.

Debt Relief Program

A debt relief program works differently from other options. Rather than taking on new credit, you work with a company like Accredited Debt Relief to consolidate your debt into a manageable payment and work with creditors on your behalf for a more favorable timeline. The goal is to resolve your debt for less than the full amount owed.

These programs are designed for unsecured debt like credit cards and personal loans. They can’t take on secured debt like mortgages or auto loans, and reputable companies won’t charge you any fees until an offer has been reached and you’ve made your first payment toward it.

Signs You Should Consolidate Your Credit Card Debt

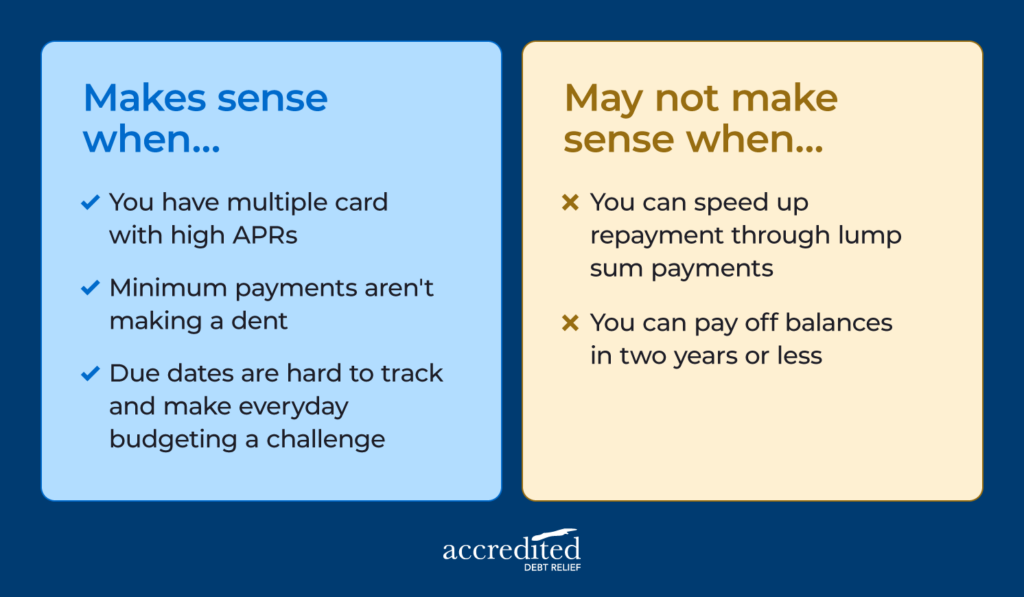

Debt consolidation isn’t the right fit for everyone, but there are clear signals that your current approach isn’t working. Recognizing them is the first step toward making a smarter decision.

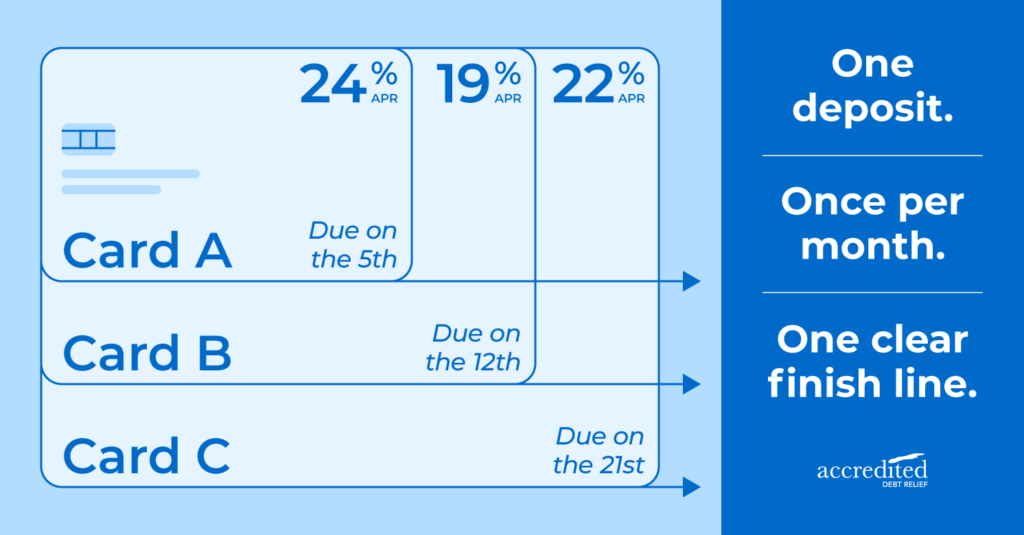

You’re Carrying Balances on Multiple Cards

When you carry balances across several cards, you are likely paying high APRs on each one at the same time. Those rates compound over time, making it harder to chip away at what you actually owe, no matter how consistently you pay.

According to the New York Fed, total credit card balances in the U.S. have risen steadily in recent years, reflecting how common this situation has become.

You Can Only Afford Minimum Payments

Minimum payments are designed to keep you current, not to help you get out of debt quickly. For example, on a $5,000 balance at 20% APR, paying only the minimum each month can take more than a decade to pay off and cost thousands in interest alone.

You’ve Missed a Due Date or Come Close

Missing a credit card payment, even once, can trigger a penalty APR that is often significantly higher than your standard rate, plus a late fee that adds to your balance immediately. If you are regularly cutting it close on due dates, consolidating into a single payment can reduce the risk of costly slip-ups.

When Consolidating Credit Card Debt May Not Make Sense

Not every debt situation calls for consolidation, and it is worth weighing the pros and cons of debt consolidation before committing. If you can realistically pay off your balances within two years through budgeting alone, consolidation may not be worth the cost. Consolidation also works best when paired with a plan to avoid adding new balances going forward.

Explore Debt Consolidation Options Through Accredited Debt Relief

If you have been asking yourself whether you should consolidate your credit card debt, you are already thinking about this the right way. Whether you are carrying a few thousand dollars across several cards or a much larger balance, understanding your options is the most important first step.

A Consolidation Specialist at Accredited Debt Relief can help you look at the full picture and determine which path makes sense for your situation at no cost to you.

Credit Card Debt Consolidation FAQ

Will I Lose My Credit Cards if I Consolidate My Debt?

It depends on the method. With a balance transfer or personal loan, your existing cards typically remain open. If you enroll in a debt relief program, you will be asked to stop using the enrolled cards during the program.

Does Credit Card Debt Consolidation Hurt Your Credit Score?

Some credit impact from using debt consolidation options is common but varies by type. For debt consolidation loans and balance transfers lenders will conduct a hard inquiry during the application process, which can impact your score. Over time, consolidating debt and making consistent on-time payments tends to have a positive effect on your credit health long-term.

Is It Better to Consolidate Credit Card Debt or Pay It Off?

If you can pay off your balances within a year or two without taking on new credit, that is often the simpler path. If high interest rates are consuming a large portion of every payment and progress feels slow, consolidating can help you pay down the principal faster overall.

Is $20,000 a Lot of Credit Card Debt?

$20,000 in credit card debt is well above the national average, but it is also a range where debt consolidation options can make a real difference. At high APRs, that balance grows quickly with minimum payments alone, which is exactly the situation where exploring your options is worth a free conversation with a Consolidation Specialist.

This content is for informational purposes only and is not financial or legal advice. Individual results will vary.