Updated July 2020

Using a credit card is a great way to establish credit and can pave the way for more advanced borrowing like a car loan, personal loan or mortgage. Unfortunately, not all credit cards have good terms and some cards come with extra fees and penalties that can be costly to the unsuspecting consumer.

This is why it is important to thoroughly understand the terms of any credit card you use and make sure that you understand how the credit card companies make money on your debt.

Credit Cards are a Revenue Stream for Lenders

We all know that financial institutions make money lending to consumers, but we often don’t think about how that cost is transferred to us, the consumer. We typically believe that interest rates and late fees are the primary revenue streams for credit card companies.

It is our responsibility as the consumers to educate ourselves on how credit card companies work. We need to know where our money is going and how to avoid credit cards with unreasonable terms that could trap us in a cycle of debt.

4 Ways Credit Card Companies Make Money

| Quick Links | |

| Merchant Fees | Merchant fees are money charged by a merchant service to a vendor for processing credit card transactions. These are typically calculated as a percentage of each credit card sale and are sometimes called interchange fees. |

| Consumer Fees | Consumer fees including any fees charged to the credit card user in association with using the card. This can include an annual fee, late fee, foreign transaction fees, cash advance fees, and balance transfer fees. |

| Interest | Your credit card interest rate is based on a percentage of your credit card balance and is accrued monthly. |

| Sales Commissions | Money made when the credit card company legally sells your data to other companies. |

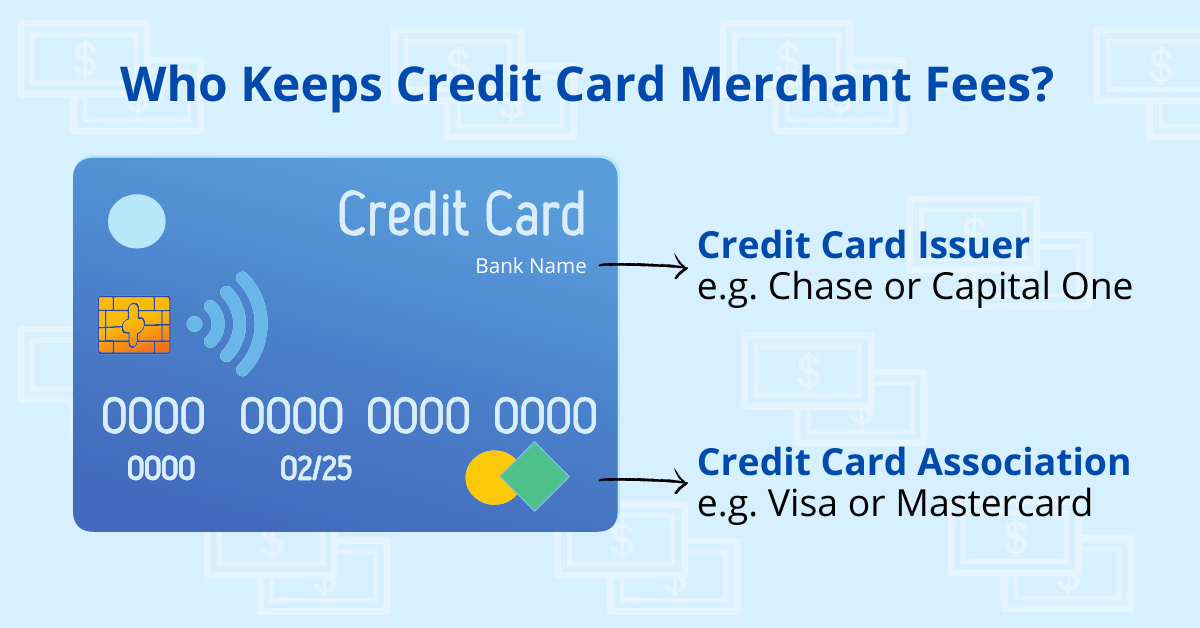

1. Merchant Fees

When you use a credit card to pay for goods and services the merchant does not get to keep the entire payment. Instead, the credit card company takes a small percentage of the sale, usually around 2 percent.

This is called a merchant fee and split between the credit card issuer and the credit card association that manages the account.

Credit Card vs. Debit Card Merchant Fees

Merchant fees, also known as interchange fees, also affect debit card use. In this care, the fee covers the same set of services. The bank takes a cut of the sale as does the credit card association that processed the transaction.

Ever wonder why not all merchants take American Express?

American Express runs a “closed-loop” network which means it acts as both the credit card issuer and the credit card association. They also charge a higher fee than most of their competitors. Merchant fees make up 65% of the total revenue for American Express, showing just how profitable they can be.

How do Merchant Fees Affect Consumers?

Interchange fees primarily impact merchants who, for example, receive only $97-$98 of a $100 credit card purchase. This can sometimes cause merchants to pass on the cost to consumers by increasing the price of goods and services. However, the merchant fee makes it possible for cash free sales, and ensures secure transactions which is a matter of convenience for both merchants and consumers.

How to Avoid Merchant Fees

If you want 100% of the money you spend to go to the merchant, skip using a credit card and pay with cash. Also, ask stores and restaurants if they charge extra fees for credit cards or if they offer discounts for cash sales.

2. Consumer Fees

Credit card companies collect fees from their customers both as regular assessments for certain services or as penalties for late or missed payments.

Typical Consumer Fees

- Annual Fees

- Balance Transfers

- Cash Advance Fees

- Foreign Transactions

- Late Fees and Penalties

Annual Fees

An annual fee is a flat rate charged once a year for use of the bank’s credit card service. This fee will be clearly stated on your credit card application and is a predictable expense.

Balance Transfers, Cash Advances and Foreign Transactions

Balance transfers, cash advance fees and foreign transaction fees only affect the consumer when they use these services. These fees are usually based on a percentage of the transaction. The percentage tends to be higher than the interest rate on the card and can add up quickly. Make sure you are selective about when you use these services and read up on the fee structure before using them.

Late Fees and Penalty APR

Paying your bill by the due date is essential. If you can, we recommend paying down your credit card balance every month, because this is great for your credit score and will help you save on interest. However, if you can’t do this, it is very important that you make your minimum payment on time.

The average late payment fee on a credit card is $36. Also, if you are more than 60 days late with a payment your credit card company might increase the interest rate on your balance. This is called a penalty APR. The average penalty APR is 21.54% but can be as high as 29.99%. This penalty can affect your credit card for up to 6 months!

Never Miss a Payment Again!

You can easily avoid late fees by automating your credit card payments! Most issuers allow you to customize your payment schedule to pay the minimum payment, current balance, or a specific monthly amount of your choosing.

3. Interest

Anytime you have an active balance on your credit card account your issuer will charge interest on that debt. Interest is accrued monthly at a regular rate. Your interest rate depends on the quality of your credit score and will be assigned when you apply for the card.

Interest is accrued monthly, but can increase as a penalty if you fail to make payments for 60 to 90 days. The average interest rate on a credit card is 18.61%.

Credit card companies make a healthy profit from the interest paid on credit cards, however, regular interest is less costly and disruptive to the consumer than late fees or a penalty APR. That is why credit card companies make it easy for you to automate your payments. They do not want you to fall behind because, even though they make money on late fees, they make more consistent revenue if you continue spending and paying on the credit card. A delinquent account is not profitable for credit card issuers.

Save Money on Interest

The best way to save on interest is to pay down your credit card balance every month. If you have poor credit, you should focus on good habits to help build or repair your credit, so you can qualify for lower interest rates.

4. Sales Commissions

Credit card companies collect data on every customer that uses their services. This includes your contact information and data on when, where and how much you spend. It’s completely legal for the credit card companies to sell this information to other lenders. That’s why you receive unsolicited mail from other lenders for loan and credit card offers.

Can I stop Credit Card Companies from Selling My Data?

Yes, but you have to opt out when you fill out the application and sometimes that is not enough to prevent your data from being shared. There are many loopholes that allow lenders to share your information even if you have opted out. Lenders can legally share your data with financial affiliates or joint marketers, even if you have requested that they not share your information.

Know Where Your Money is Going

Credit card companies are for profit businesses. They make money on their services and will try to do so in as many ways as they can. While there are regulations that guard against predatory lending, it’s important for consumers to understand the terms of any debt they take on. Understanding how credit card companies make money will help you identify reasonable and unreasonable terms so that you can make informed decisions about taking on new debt.