Most people don’t set out to accumulate $100,000 in debt. It just happens. A mortgage here, a car payment there, a few months of leaning on credit cards, and suddenly the balance is overwhelming.

Debt is one of those topics most people avoid talking about, which makes it easy to assume you’re the only one struggling. But you’re not. Knowing how your debt compares to others can help you spot what’s manageable, what’s worth prioritizing and where you might need outside help.

Here’s what the numbers look like across each major debt category.

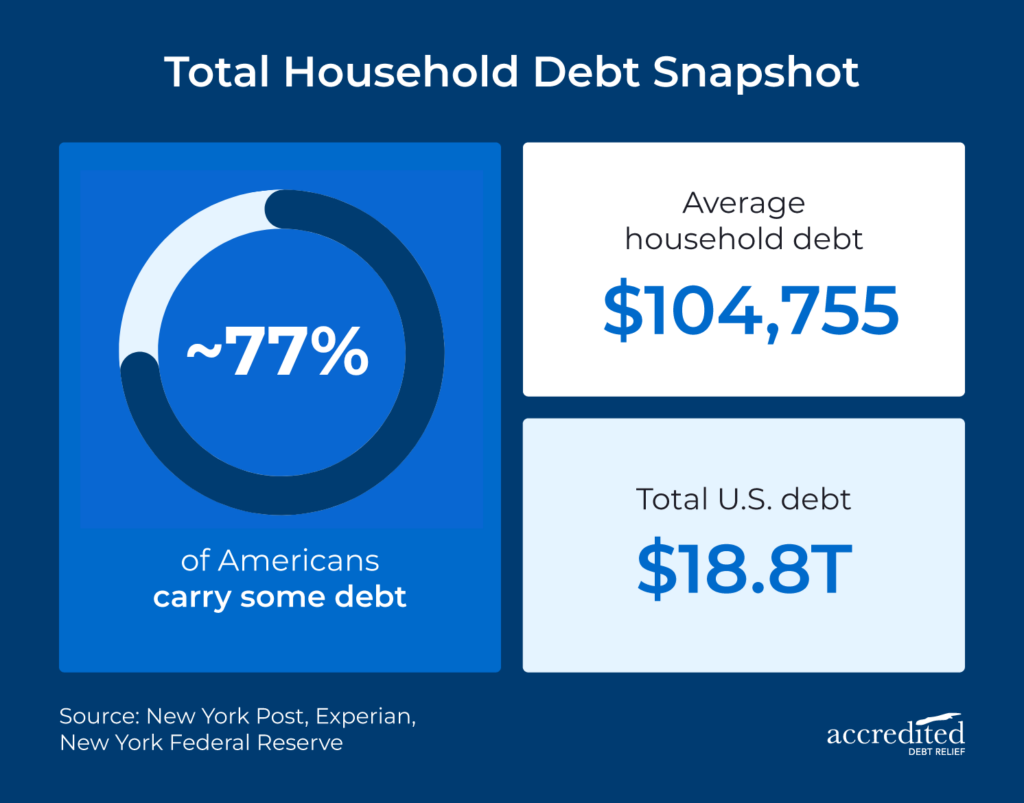

- • Total U.S. household debt reached a record $18.8 trillion in Q4 2025, per the New York Fed.

- • The average American household carries $104,755 in total debt, per Experian.

- • Mortgage balances account for roughly 70% of all household debt at $13.17 trillion, according to the New York Fed.

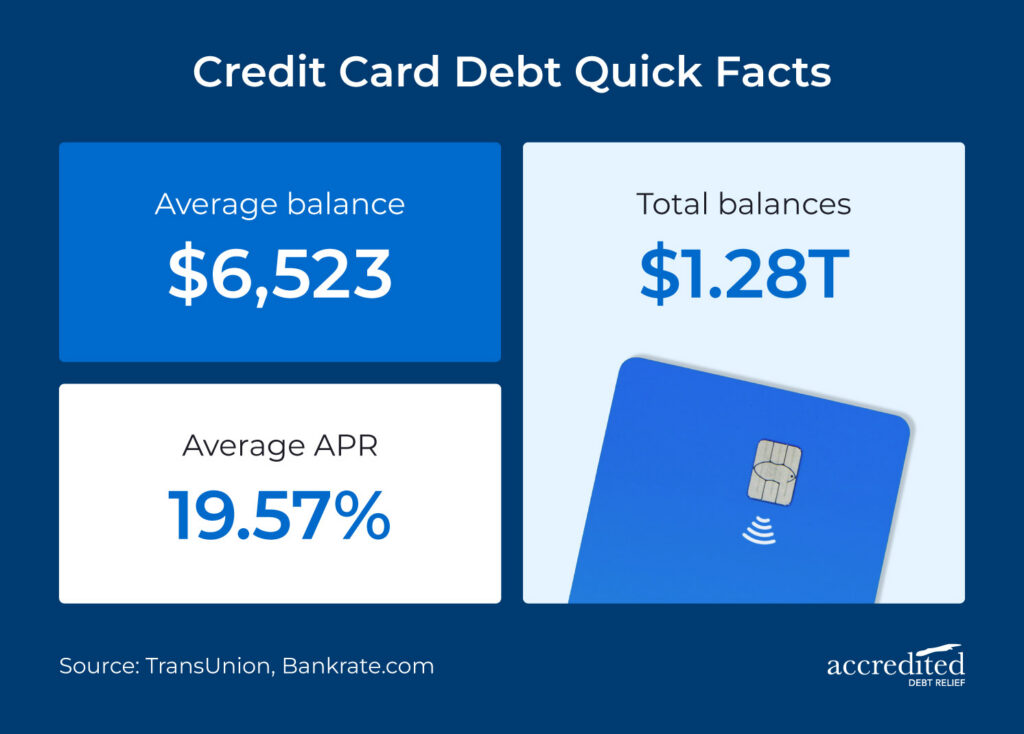

- • The average credit card balance is $6,523 per borrower, with APRs averaging 19.57%, per TransUnion and Bankrate.

- • The average auto loan balance is $24,602, with new car payments averaging $748/month, per TransUnion and Experian.

- • The average student loan borrower owes between $37,400 and $43,300, per Education Data Initiative.

- • About 77% of Americans carry some form of debt, and delinquency rates are at their highest since 2017, per the Federal Reserve Board and New York Fed.

Total American Household Debt

Total U.S. household debt reached $18.8 trillion in Q4 2025, according to the New York Federal Reserve, a record high. When you spread that across American borrowers, Experian puts the average American household debt at $104,755 as of mid-2025.

Those numbers reflect something important: Debt is a near-universal experience. About 77% of Americans carry some form of debt, according to reporting from the Federal Reserve Board. That means if you’re managing multiple balances or feel stretched thin by payments, you’re far from alone.

For many households, debt isn’t a sign of poor decisions. It’s the result of navigating rising costs, major life milestones and an economy that increasingly runs on credit. And while carrying a balance is common, every type of debt comes with its own risks.

The U.S. National Debt vs. Household Debt

The two figures often get conflated in headlines, but they measure completely separate things.

| National Debt | Household Debt | |

|---|---|---|

| What it is | What the federal government owes | What individual Americans owe |

| Current figure | ~$38 trillion (Oct 2025) | $18.04 trillion (Q4 2024) |

| Per person | ~$111,262 | Varies by individual |

| Examples | Government bonds, Treasury bills | Mortgages, credit cards, student loans, auto loans |

Source: U.S. Treasury Fiscal Data

Average American Mortgage Debt

According to the New York Fed’s Q4 2025 report, total mortgage balances stand at $13.17 trillion, roughly 70% of all household debt in the country.

On an individual level, TransUnion puts the average mortgage balance at $268,060, with a median monthly payment of approximately $2,025 as of December 2025, per the Mortgage Bankers Association. Home equity lines of credit (HELOCs) have also climbed for 15 consecutive quarters, reaching $434 billion as of Q4 2025, according to the New York Fed.

A mortgage is often called “good debt” because it builds equity and typically carries lower interest rates than other loan types. But for homeowners also carrying unsecured debt, the combined monthly obligations can create real cash-flow stress.

Average American Credit Card Debt

Credit card debt is where many Americans feel the most financial pressure, and it’s easy to see why. Total credit card balances hit $1.28 trillion in Q4 2025, according to the New York Fed. The average American credit card debt per borrower was $6,523 in Q3 2025, per TransUnion.

What makes credit card debt particularly costly is the interest rate attached to it. With average APRs at 19.57% as of April 2026 (per Bankrate.com), paying only the minimum can quietly extend your debt timeline by years.

Average American Auto Loan Debt

Auto loans now rank as the third-largest household debt category in the U.S. Total auto loan balances reached $1.67 trillion in Q4 2025, according to the New York Fed. Experian’s Q3 2025 data puts the average American auto loan balance at $24,602.

Monthly payments reflect how much car costs have risen in recent years. The average new car payment was $748 per month in Q4 2025, while the average used car payment was $532 per month, according to Experian. Interest rates have added to the burden: New car APRs averaged 6.36% while used car loans averaged 11.40% in Q3 2025, per Experian Automotive data.

Longer loan terms, such as 72- and 84-month agreements, have become more common as dealers try to make high sticker prices feel manageable month to month. The tradeoff is that borrowers often end up paying significantly more in interest over the life of the loan.

Average Student Loan Debt in America

Student loan debt affects more than 43 million Americans, and the balances are significant. As of early 2026, the average borrower carries between $37,400 and $43,300 in student loan debt, according to Education Data Initiative and Investopedia analyses of 2024–2025 data.

Repayment hasn’t always kept pace with those balances. Starting in Q1 2025, previously unreported missed federal student loan payments began appearing in credit reports. The serious delinquency rate jumped sharply as a result, reaching 7.74% of aggregate student debt, according to the New York Fed.

Student loan debt remains one of the most complex and fast-changing pieces of the household debt picture.

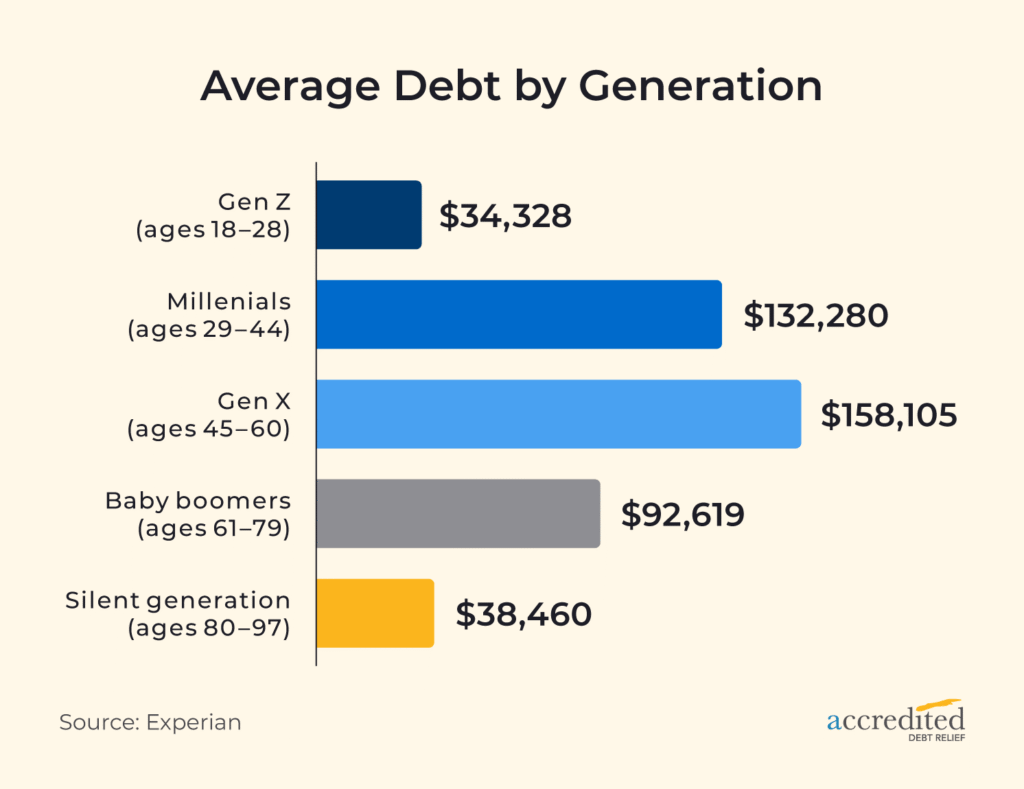

How Debt Varies by Generation

Debt doesn’t look the same at every stage of life. Experian’s data shows average consumer debt varies widely by generation:

Adults between 40 and 49 carry the most total debt, about 4 times more than adults between 18 and 29, according to the New York Fed’s Consumer Credit Panel. Millennials carry the highest average mortgage debt, while Generation X leads in credit cards and auto loans.

While Generation X leads in average credit card debt, there has been a notable rise in Gen Zers with credit card debt in recent years, with balances growing 15.35% in 2023 alone, according to Experian.

Debt Delinquency by the Numbers

Rising debt levels have come with a rise in delinquencies. According to the New York Fed, 4.8% of outstanding debt was in some stage of delinquency as of Q4 2025, up from 3.6% a year earlier and the highest rate since Q3 2017. Transitions into serious delinquency increased for credit card balances, mortgages and student loans during the quarter.

These trends reflect economic pressures that are affecting millions of households, not just individual missteps. Rising costs, stagnant wages and higher interest rates have made it harder for many people to stay current even when they’re doing everything right. If your payments are becoming difficult to manage, knowing your options early gives you more of them.

Explore Alternatives With Accredited Debt Relief

Carrying significant debt can make the future feel uncertain, but the numbers show you’re far from alone. If you’re dealing with high-interest unsecured debt, there are more options than you might think to help you get ahead of it.

Get your free consultation from a Consolidation Specialist at Accredited Debt Relief. They’ll walk through your debt consolidation options with no obligation to enroll.

The content and resources provided are for informational purposes only and do not constitute legal, tax, or financial advice. Accredited Debt Relief will not be responsible for the accuracy of the information contained or provided on this site, or for the consequences of any reliance on such information. Individual results may vary.

Sources

- New York Fed Q4 2025 Household Debt and Credit Report: newyorkfed.org

- Experian Average American Debt by Age: experian.com

- U.S. Treasury Fiscal Data (National Debt): fiscaldata.treasury.gov

- TransUnion Q3 2025 Consumer Credit Report: newsroom.transunion.com

- Mortgage Bankers Association (via Motley Fool): fool.com

- Experian 2025 Consumer Debt Study: experian.com

- Experian 2025 Consumer Credit Review: experian.com

- Experian Average Monthly Loan Payment: experian.com

- Bankrate (Credit Card APR): bankrate.com

- Federal Reserve: federalreserve.gov

- Education Data Initiative: educationdata.org

- New York Fed Q1 2025 Student Loan Delinquency Report: newyorkfed.org