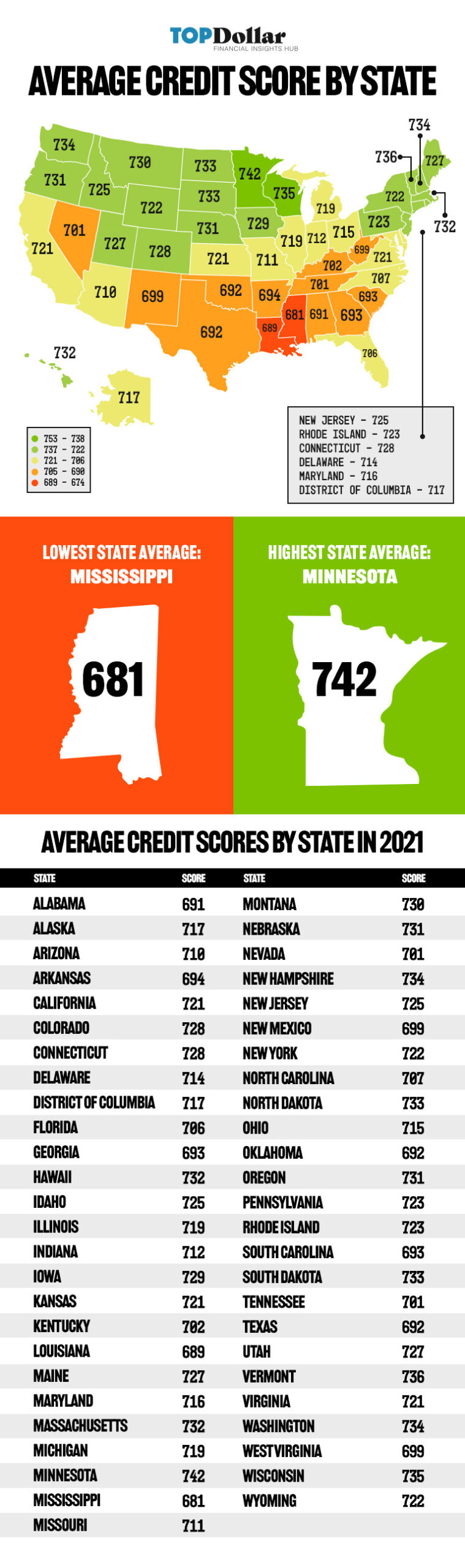

You probably know your credit score, but have you ever wondered how your score compares to others in your state? After another year of economic uncertainty, credit scores have fluctuated but not in the way you might expect. Credit scores across the country are up! Check out our summary of the 2021 FICO score data from Experian.

Credit Score Basics

Your credit score is a three-digit number used by lenders, landlords, and other institutions to determine your creditworthiness and ability to make payments. Credit scores are generated by credit bureaus with scoring models that consider factors like your payment history, credit utilization, account age, credit mix and recent applications.

National Average Credit Scores Increased in 2021

According to Experian, the average credit score increased between 6-10 points in 2021 for two major scoring models: VantageScore and FICO. This increase is part of a decades-long trend that has shown an increase in average credit scores.

| Year | VantageScore | FICO Score |

| 2021 | 698 | 716 |

| 2020 | 688 | 710 |

| 2019 | 682 | 703 |

| 2018 | 680 | 705 |

| 2017 | 675 | 701 |

| 2016 | 680 | 699 |

| 2015 | 699 | 695 |

| 2014 | 697 | 692 |

| 2013 | 696 | 691 |

| 2012 | 695 | 690 |

| 2011 | 694 | 688 |

Why Are Average Scores Increasing?

Despite economic hardship, average credit scores continue to increase year over year. The result may seem ironic however, there are plenty of reasons why scores did not suffer as much as you might expect.

Americans have managed to improve their credit scores because:

- Financial literacy is at an all-time high thanks to online educational resources.

- More Americans focus on credit score as a measure of financial wellness and attend to behaviors that will keep their scores healthy.

- Lenders are willing to work with consumers to accommodate changes in payment such as forbearance, changes to terms and lower monthly payments.

- Enhanced unemployment benefits and stimulus payments helped Americans pay down debt during the pandemic.

What Is a Good Credit Score

Credit score ranges differ slightly depending on the scoring model used. For FICO scores, which are used by 90% of lenders to determine creditworthiness, the following breakdown is applied.

- Poor: 300 to 579

- Fair: 580 to 669

- Good: 670 to 739

- Very good: 740 to 799

- Excellent: 800 to 850

A good credit score is any 670 and above, scores 669 and below are considered fair or poor.

Why Do Credit Scores Matter

Credit scores are not the only measure of financial health but they do serve an important purpose. Credit scores provide context for institutions who want to assess your ability to pay on current and future debts.

For example, if you are trying to take out a loan, take on a mortgage, or buy a car your credit score will affect the amount of money you can borrow and the interest rate available to you. Higher scores will always be better but the minimum thresholds vary depending on the type of debt.

Very poor scores may affect your ability to borrow at all, or limit how much you are allowed to borrow. Higher scores can also unlock more favorable interest rates that will save you money.

Likewise, credit scores and reports are often used by landlords or employers to gauge your financial behaviors. Having a very poor score could affect your apartment or job application.

How To Improve Your Credit Score

Improving your credit score is more straightforward than you may think because scoring models are predictable and reward certain behaviors. To improve or repair your score, you need to analyze your current score, identify your weaknesses and implement the actions and behaviors that will move the needle in your favor.

Depending on the type of weaknesses on your report, changes can happen within a few months, or may take several years for more permanent or significant recovery.

Learn more about six habits you can adopt that will help you repair your credit score.