One trip to the ER or one unexpected procedure is all it takes to rack up a medical bill you can’t easily cover. It’s a struggle millions of people know firsthand, with the Kaiser Family Foundation putting the number at roughly 100 million Americans carrying some form of health care debt.

How medical debt shows up on your credit report has changed in recent years, and several of those changes can work in your favor. The rules are still shifting, though, so it helps to know which protections are in place today and how to use them.

Does Medical Debt Affect Your Credit Score?

Medical debt usually doesn’t affect your credit score right away, and it often doesn’t at all. Hospital bills don’t affect your credit the way a credit card does, because hospitals and doctors’ offices don’t report to the credit bureaus directly.

A medical bill on its own won’t appear on your credit report, and an unpaid balance only becomes a credit problem if it goes to a collections agency. That said, protections vary by state, so it’s worth knowing the rules where you live.

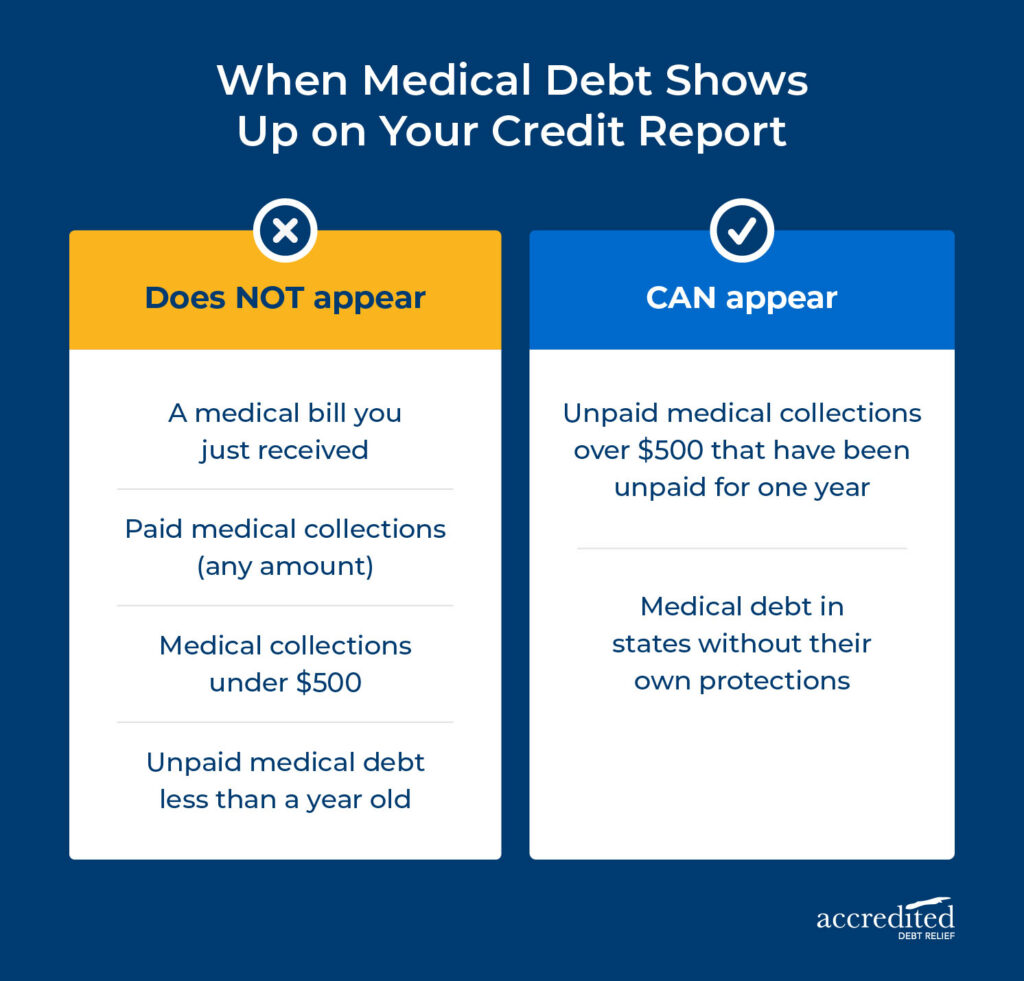

How Long Does Medical Debt Stay on Your Credit Report?

Medical debt can stay on your credit report for up to seven years, counted from the date of the first missed payment. But thanks to voluntary changes the three major credit bureaus adopted in 2022 and 2023, it may affect you for less time, or never show up at all.

First, paying off a medical collection clears it from your report. Equifax, Experian and TransUnion now remove paid medical collections regardless of the balance, so how long medical debt stays on your credit often comes down to whether you’ve resolved it.

Second, you get more time before an unpaid bill appears at all. Unpaid medical collections now wait a full year before they can show up on your credit report, giving you a window to sort out insurance issues, billing errors or a payment plan.

How Recent Medical Debt Credit Reporting Rules Affect You

For most people, these changes mean medical debt on a credit report is far less likely to drag down a score than it was a few years ago, especially smaller balances and bills you’ve already paid.

There’s a catch worth knowing, though. Most of these protections are voluntary policies the credit bureaus adopted, not federal law, and a 2025 court decision struck down a federal rule that would have gone further. So it helps to know where things stand and how to use the protections you have.

Start by pulling your credit reports from all three bureaus and checking how any medical debt is listed. If a collection is paid, under $500 or simply inaccurate, it shouldn’t be there, and you can dispute it to have it corrected or removed.

Larger unpaid balances are different, since the current rules don’t remove them and they can still affect your score. If medical bills are piling up alongside credit cards or other debt, options like debt relief programs and debt consolidation loans may help you manage multiple unsecured debts more simply.

How To Handle Medical Debt That’s Hurting Your Credit

You still have options if your medical debt has already gone to collections and landed on your credit report. These practical steps can help you limit the damage and work toward getting it resolved.

Check your credit report for errors

Medical debt errors are more common than you might expect. Billing mistakes, misapplied insurance payments and duplicate accounts can all show up on a credit report incorrectly, and any one of them could be lowering your score for the wrong reasons.

Start by requesting your free credit reports at AnnualCreditReport.com, where you can pull all three bureaus. Review how any medical debt is listed and compare it against your own bills and insurance statements. If something doesn’t match, dispute it directly with the bureau reporting it, and confirmed errors must be corrected or removed.

Work directly with the provider

It is worth calling the billing department directly and asking what options are available. Many hospitals and medical providers offer financial hardship programs, and some will accept a reduced amount to resolve a bill rather than keep chasing the full balance.

Providers are often willing to accept a lower amount or set up a payment plan you can manage. Ask for any agreement in writing before you pay, so the terms and the credit reporting impact are clear.

Explore debt consolidation options

Because medical debt is unsecured, unlike a mortgage or car loan that’s backed by property, it can be folded into debt consolidation options. That’s an umbrella term covering a few different approaches:

- Debt relief program: Works with your creditors on your behalf to manage enrolled debts, often combining medical bills with other unsecured balances, and lowering your monthly payment.

- Debt consolidation loan: Rolls multiple debts into one new loan with a single monthly payment.

- Balance transfer credit card: Moves your balances onto one card, sometimes with a lower introductory rate.

See What Debt Relief Alternatives Are Available to You

Wherever you are with your debt, getting a clear sense of your options is a good place to start. Accredited Debt Relief can help you explore debt consolidation options built around your situation.

FAQ

Will paying off medical debt improve my credit score?

Paying off medical debt can improve your credit score, but results aren’t guaranteed. The three major credit bureaus remove paid medical collections from your report, so clearing the balance can lift that negative mark. The effect varies by person and by which credit scoring model a lender uses.

Can I be sued for unpaid medical debt?

Yes, you can be sued for unpaid medical debt. Like other unsecured debts, an unpaid medical bill can be turned over to collections, and a provider or collections agency can take legal action to recover what is owed.

Does medical debt affect your ability to get a loan?

Medical debt can affect your ability to get a loan, though often less than other debt types. Because smaller and paid medical collections no longer appear on your report, much of it may not affect a loan application at all.

The information on this site is provided as a general resource and does not constitute legal, tax, or financial advice. While Accredited Debt Relief strives to ensure accuracy, this content, including any third-party sources referenced, should not be the basis for any financial decision. For guidance specific to your situation, we recommend consulting a qualified professional.