One of the hardest parts about paying off multiple debts is knowing where to start. It can be easy to become overwhelmed by or apathetic to minimum payments. Unfortunately, this leads to being in debt longer and racking up interest and fees. Reprioritizing your debts and pursuing a repayment strategy can help increase your long-term savings and motivation. Two of the most common debt repayment methods are the snowball method and the avalanche method. Although they’re similar in many ways, they can lead to very different results – which one is best for you?

Why Any Strategy Is Better Than None

Time and money can quickly go to waste when you don’t approach your debts with a plan in mind. Analyzing your balances can help you clarify exactly what you owe, and creating a set repayment plan can help ease stress and uncertainty.

This is especially important if your funds are combined with those of your partner or spouse – without a unified strategy, you may find yourself working much harder to reduce your balances while your partner’s spending leads to increased debt. By mapping out your finances and discussing strategies together, you can avoid money miscommunications and tackle your debt as a team.

Avalanche Method

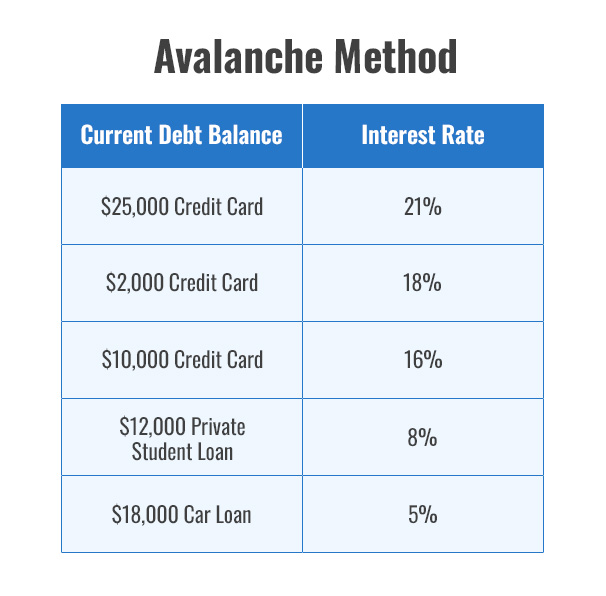

If you’re hoping to pay the least amount of interest as possible, the avalanche method may be the most appealing to you. To begin this strategy, make a list of all of your debts, ordering them by interest rate. Here’s an example:

For every debt except for the one at the top of your list, you’ll make the minimum payment. As for the highest interest rate debt, you’ll put as much money as you can towards that debt every month. Once you’ve finished paying off that debt, you’ll move all of the additional funds that you were putting towards your priority debt towards the debt with the next highest interest rate, and you’ll continue to make minimum payments on the rest. This process is continued until all debts have been paid off.

Since this strategy tackles the debts with the highest interest rates first, it should theoretically save you the most. Unfortunately, due to the design of this plan, it can take more time to tackle the first debt and see the “avalanche” take momentum. The initial lack of results can be discouraging, so it’s important to find other ways to stay motivated if you pursue this strategy.

Snowball Method

Unlike the avalanche method, the snowball method focuses on your lowest balances first. This strategy allows you to knock out smaller debts earlier on, which can help fuel your motivation as you work towards your largest debt.

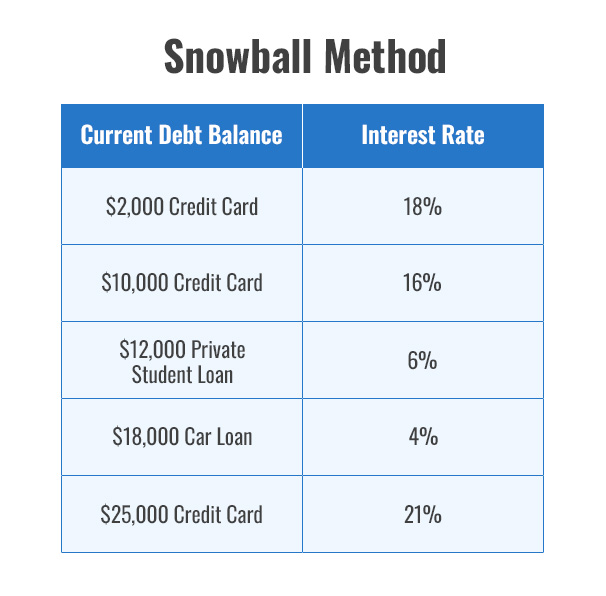

To start with the snowball method, order your debts from the lowest balance to the highest balance. Using the example above, we’ve reordered the same debts based on size rather than interest rate:

According to the snowball method, the $2000 credit card debt should take the highest priority. The rest of the debts on the list will receive the minimum monthly payment while extra payments are made towards the highest priority debt. Once the highest priority debt has been fully paid off, you’ll roll those payments towards the next smallest debt on your list while paying minimums on the rest. This process will continue until all debts on the list are paid off.

Rather than fixating on interest rates, the snowball method focuses on “easy wins” that can help motivate you along the way. This effect is similar to the satisfaction you feel when playing video games or puzzle games – victories in easier levels in the beginning help you stay driven to complete the hardest level at the end.

Which Method Is Better?

Debt solutions are not “one size fits all,” and the level of success you’ll have with either of these methods depends on your personal views, monetary behavior and motivation level.

If you’re someone who struggles with motivation, the faster results from the snowball method might be best for you. Although you may pay more interest in the long run, you’ll be able to vanquish smaller debts early on and cross them off your list, which can provide the momentum you need to keep going. This is also the method that most financial experts recommend over the avalanche method. Although the final results aren’t as mathematically appealing, most people benefit more from the quick wins and have an easier time sticking with it.

If you can stay motivated for a longer period of time and are willing to sacrifice early on victories in order to save in interest, the avalanche method will be better for you. It’s important to stay patient and driven if you go with this strategy. Try creating a visual reminder of your progress, and consider asking a trusted friend to be your accountability partner.

Other Debt Repayment Strategies

The snowball and avalanche methods aren’t your only options when it comes to paying off debt. You may choose to prioritize your debts based on emotional impact instead of by balance or interest rate. Others have found success using a combination of both the avalanche and snowball methods, making a unique priority list that makes the most sense to them. If your debts are too overwhelming to address on your own, you may benefit more from a professional debt consolidation service.

In the end, motivation is the biggest factor when it comes to paying off debt. If you consistently make more than your minimum payments, look for additional ways to save, and avoid taking on additional debt, your hard work can lead to major results.