Updated May 10, 2023

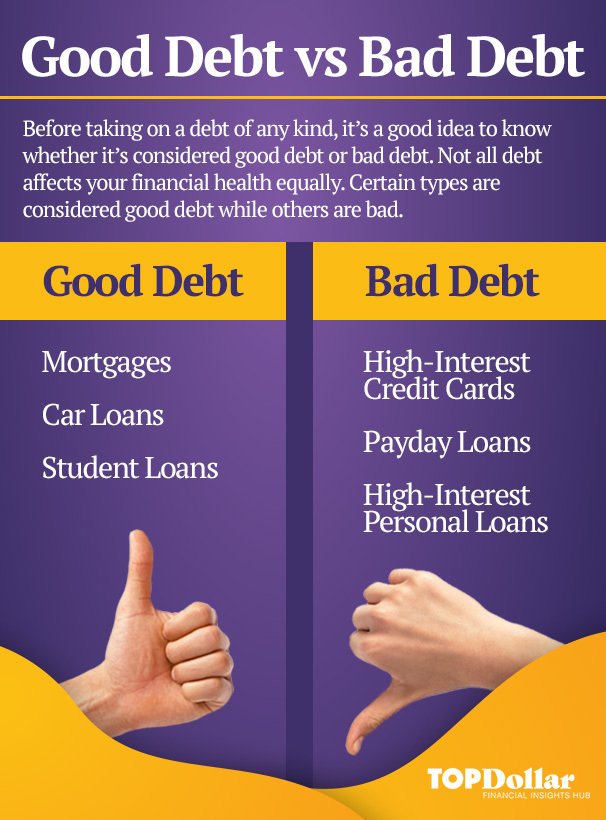

Before taking on a debt of any kind, it’s a good idea to know whether it’s considered good debt or bad debt. Not all debt affects your financial health equally. Certain types are considered good debt while others are bad.

Credit card debt, for example, is usually considered bad debt, as are other types of high-interest debt like payday loans and cash advances. On the other hand, mortgages, car loans, and student loans are generally considered good debt. However, there are always exceptions to these rules, if certain criteria are met.

What is Good Debt?

Good debt is any sort of debt that carries a low-interest rate and will increase your net worth.

3 Examples of Good Debt

- Mortgages

- Car loans

- Student loans

When these debts are paid, you end up with an object or a skill that has value and could increase your net worth over time. Mortgages and Car loans are secured debt.

Mortgages

Buying a house is one of the most important financial decisions that most people make in their lifetimes. Home loans traditionally have very low-interest rates, with an average of 2.5% to 8.75% from banks and 3% to 4% from credit unions, because the loan risk is much lower for the lender. However, the 2008 mortgage collapse was a cautionary tale about subprime borrowing. A home loan is a good debt if you can afford it! You put yourself at risk if you borrow beyond your means.

Red flags:

- Mortgage payments that are more than 36% of your total income

- You don’t have money for a down payment

- Mortgage insurance requirements, this money is a penalty for at-risk borrowers and isn’t invested in your property

Car Loans

Car loans narrowly make the good debt list because they are secured debt. They are also a necessity for most people. Many rely on their vehicles to get to work and for everyday life. The key is to make sure that you buy a car that is within your means and is worth what you’ll be paying for it. Your car payment should be 20% or less of your take-home pay.

Red flags:

- Car payment is more than 20% of your take-home pay

- You don’t have money for a down payment

- Your loan terms are greater than four years.

Student Loans

Student Loans are considered an investment in your future, but schools are becoming more and more expensive and grads often find themselves in financial trouble when their loan totals exceed their future earning potential. To avoid taking on more student loan debt than your future self can afford, crunch the numbers and aim for a monthly payment that is 8% or less than your future expected earnings.

Red flags:

- Private student loans with unregulated interest rates

- Student loan totals that exceed your future earning potential

- Using student loan money to cover expenses above and beyond tuition

What is Bad Debt?

Bad debt is high-interest debt that will not increase your net worth but instead will cost you more money long term. Bad debt is also any type of debt that is more than you can afford to pay. Good debt can become bad debt if you borrow beyond your means or exceed recommended limits on your debt-to-income ratio.

3 Examples of Bad Debt

- High-Interest Credit Cards

- Payday Loans

- High-Interest Personal Loans

High-Interest Credit Cards

Credit card interest rates are based on your credit score. The better your score the lower your interest rate will be. Any card with an interest rate over the average 15.13% is considered high. Some high-reward credit cards (miles, cashback, etc.) have high-interest rates but may be worth having if you are prepared to pay down the balance regularly. As a rule of thumb, you want to keep your debt-to-income ratio below 28%.

Possible Exceptions:

- Using a high-interest card for valuable rewards and paying it down monthly

- Store cards for promotional savings

Payday Loans

Payday loans are short-term loans with very high-interest rates. Dwarfing all other types of debt, payday loans can have APRs of up to 400% according to a warning by the Consumer Financial Protection Bureau (CFPB.) Unfortunately, people who turn to payday loans often have systemic financial struggles that make it impossible for them to pay off this type of debt.

There are no exceptions that would make a payday loan good debt, however, there are some circumstances that could warrant the emergency use of a payday loan.

Exceptions for Emergency Use:

- Ensure your physical safety or the physical safety of someone else

- Cover a medical emergency

- Paying overdraft fees

- Emergency travel

High-interest Personal Loans

Personal loans with high-interest rates meet most of the criteria for bad debt. They are costly and can damage your financial health if mismanaged. It’s generally not a good idea to take out high-interest personal loans for non-essential spending like vacations or new clothing.

Possible Exceptions:

- A high-interest loan with short-term, monthly payments than you can afford could be a viable option for big-ticket essentials like car or appliance repairs.

Struggling with Debt?

If you have fallen behind on paying back your debt, good or bad, you should consider your options. Speaking with Accredited Debt Relief can help. Call for a free consultation and speak with our specialists to discuss your options.